Why German Automakers Lost Their Home Market

West wants cheap cars. Asia invests in software. Deloitte study reveals the divide...

Welcome to Issue #103 of The German Autopreneur.

Picture this: You're in a meeting. Someone puts a new Deloitte study on the table. 29,000 car buyers across 27 countries.

Someone asks: "What drives purchase decisions in Germany vs. China?"

Most people guess: Chinese buyers chase low prices. Germans pay for quality.

The reality? Exactly opposite.

54% of Germans say price is their top criterion. In China? Only 20%.

In China, quality is almost twice as important as price.

Today we look at Deloitte's Global Automotive Consumer Study 2026. What really matters. Where we got it wrong. What it means.

Germans Want a Bargain

Germans buy primarily on price, not quality. In China, quality matters twice as much as price.

This year, the trend got even stronger.

62% of Germans say "getting a good deal" is critical when buying a car. They want to feel they got the better deal than others.

Getting a good deal is a top priority in Germany (Deloitte)

The UK and US are similar. In China, only 32% care about getting a good deal. In India, 40%.

And it continues. 25% of Germans want to spend max €15,000 on their next car. Last year: 22%. Willingness to spend €50,000+ dropped from 15% to 12%.

Price is the number one factor in Germany, performance and quality in China (Deloitte)

Here's what stands out. Germany and Japan are the ONLY markets where price matters more than quality.

In all other 25 markets, quality leads.

In China, quality (38%) is almost twice as important as price (20%). Even more important: vehicle performance at 40%. That primarily means efficiency and range.

The problem for German automakers: their home market grows increasingly price-sensitive. At the same time, Chinese competitors push into Europe with affordable EVs.

In China, it's reversed. Customers don't want the cheapest car. They want better technology. Better performance. Better features.

The Big EV Wave Isn't Coming

At least not how everyone expected.

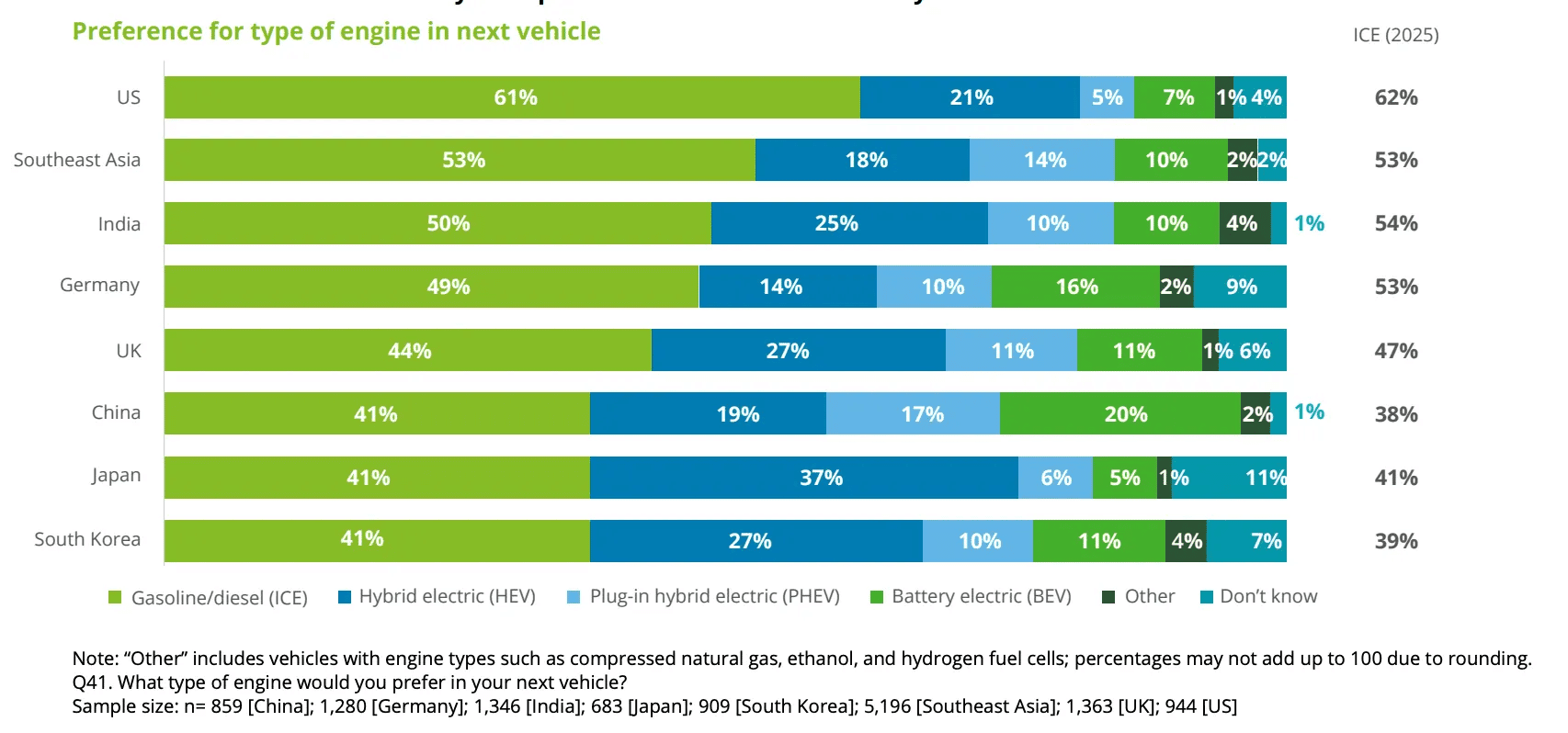

In Germany, 49% want a combustion engine for their next car. 16% want a pure EV. Sounds low, but it's the second-highest globally after China.

Even in China, only 20% want a pure EV. 41% still prefer combustion engines.

Hybrids are gaining ground, the share of combustion engines is slowly declining (Deloitte)

In the US: 61% combustion preference. The highest worldwide. Only 7% want an EV.

Japan and South Korea sit at 41%, on par with China.

But where's the shift going? Not to EVs. To hybrids.

In Germany, 24% want a hybrid (14% HEV + 10% PHEV). In China: 36% (19% HEV + 17% PHEV).

Hybrids remain an important bridge technology. The compromise more customers accept.

But why don't customers want EVs?

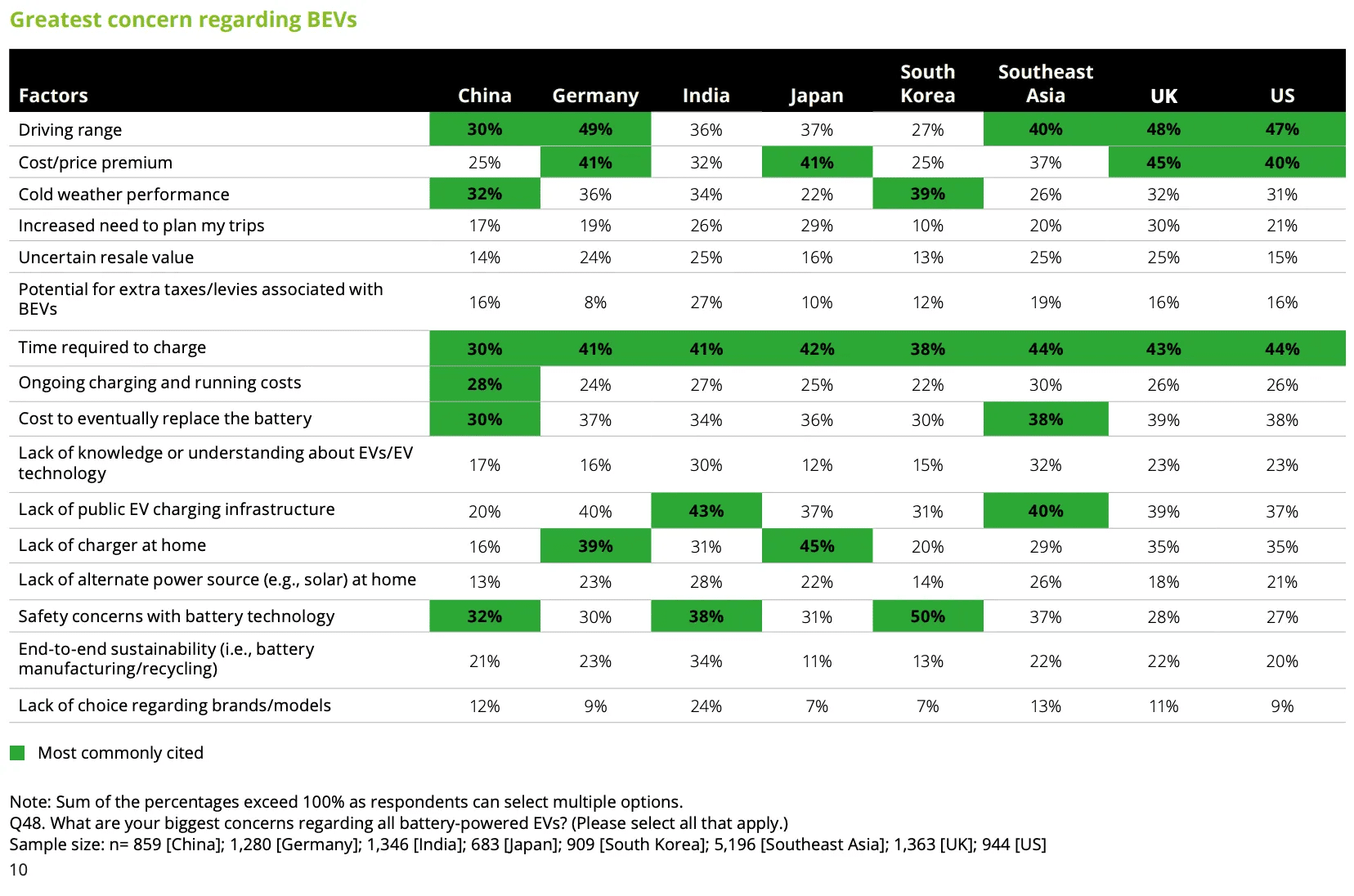

In Germany: Still range. 49% cite it as a problem. Then costs and charging time (both 41%)

In China: Different concerns. How the car performs in cold weather (32%). Whether the battery is safe (32%)

Costs are the biggest EV concern in the West (Deloitte)

Then there's the infrastructure problem.

In the UK, 79% want to charge at home. But 52% have no access to a charger. In the US: 53%. In Japan: 75%.

The gap: Customers want home charging. But they can't access it.

Germany stands better on charging infrastructure. Only 20% lack home charging access. Still, as long as this gap exists, hybrids remain the pragmatic choice.

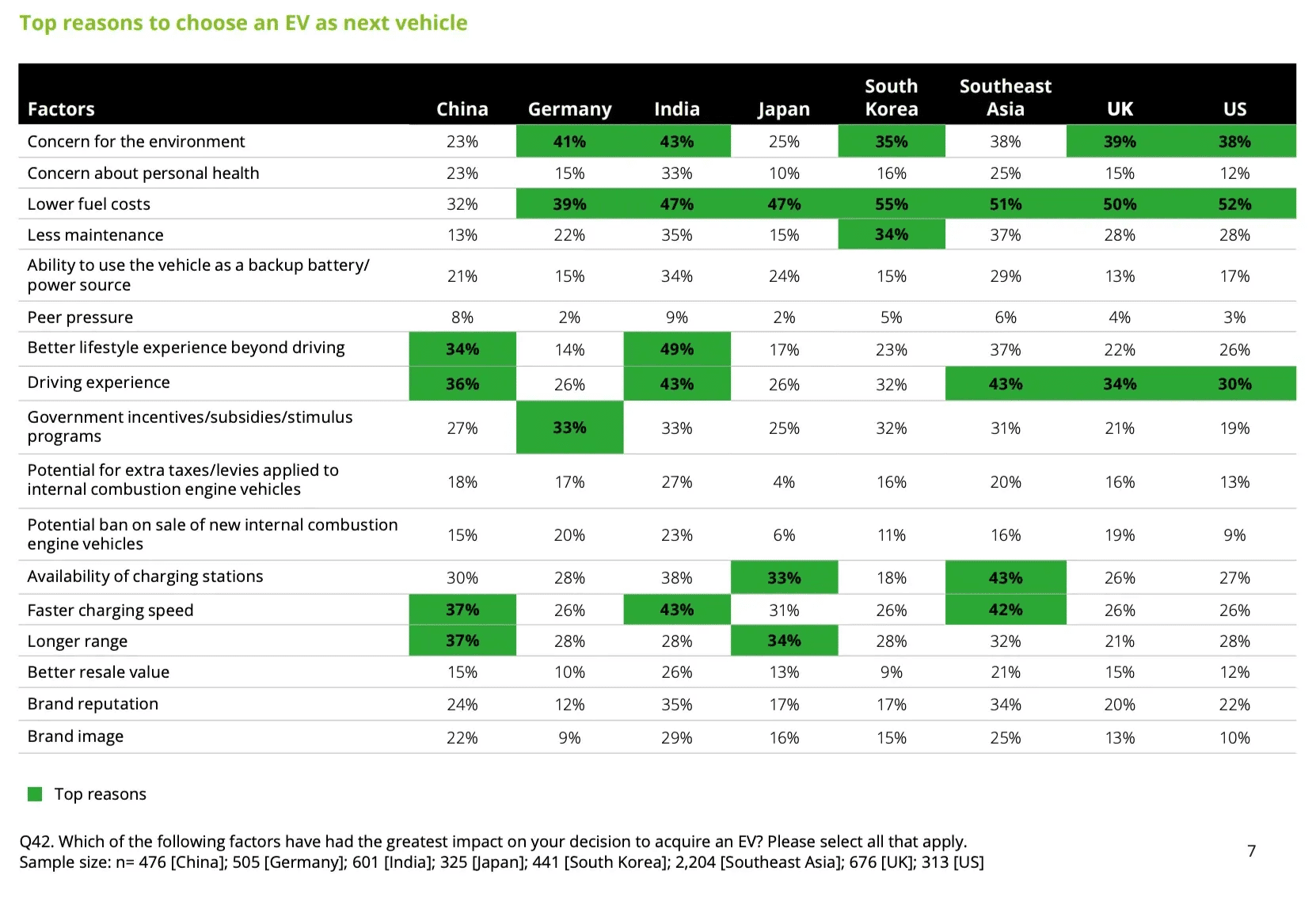

And what are the reasons for buying an EV?

Massive regional differences.

Germany: Main reason is environment (41%). Then lower fuel costs (39%) and government subsidies (33%)

China: Faster charging (37%), higher range (37%), driving experience (36%), or as a lifestyle asset (34%)

US and Japan: Lower operating costs (US: 52%, Japan: 47%)

Reasons for buying an EV: Environment in Germany, Experience in China (Deloitte)

This explains why hybrids are attractive. They offer the best of both worlds. No dependency on charging infrastructure. Lower consumption. A gradual entry into electric mobility.

The Software Gap Between West and East

Here it gets interesting.

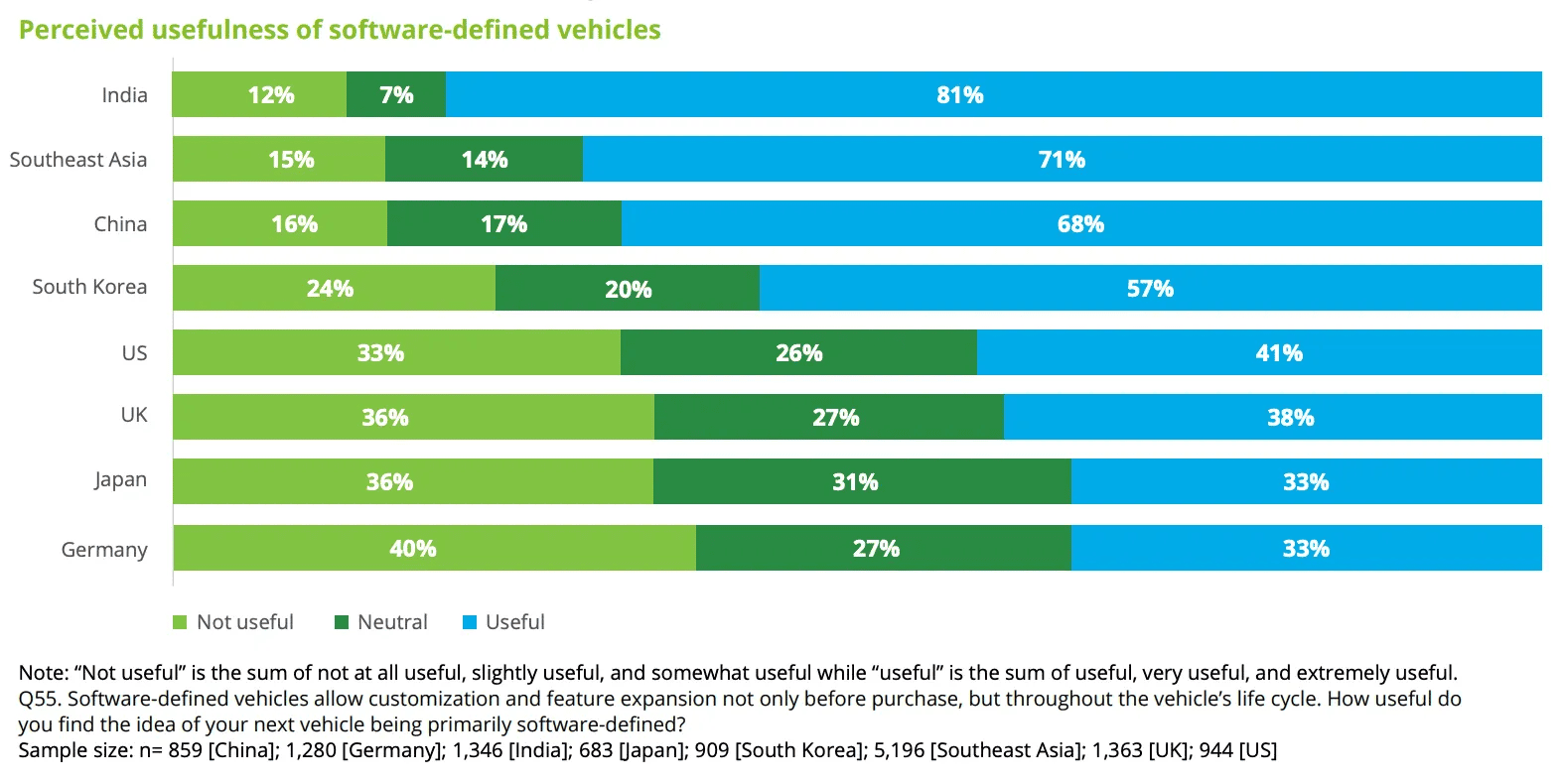

Deloitte asked: How useful do you find software-defined vehicles? The answers couldn't be more different.

India: 81% find SDVs useful. Southeast Asia: 71%. China: 68%.

At the bottom: Germany and Japan. Both at only 33%.

SDV acceptance: Asia vs. Europe diverges (Deloitte)

It's even clearer with AI features in cars.

84% of Indians would use them. In China, 76%. Southeast Asia, 70%. And Germany? 34%.

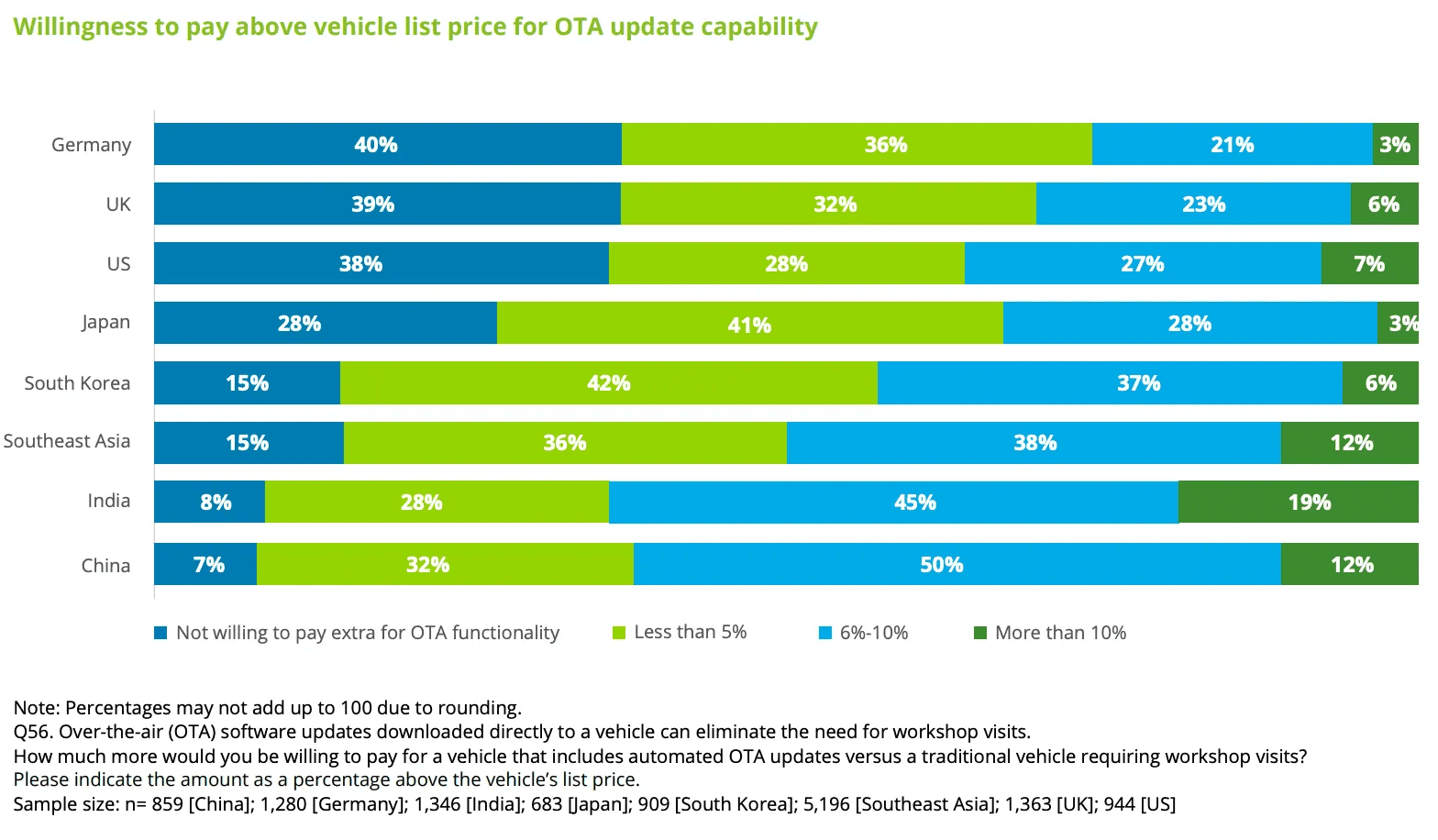

The divide becomes clear when looking at over-the-air updates and willingness to pay.

China: 93% would pay extra for OTA capability

India: 92%

Germany: Only 60%

Germans expect OTAs to be free, Chinese are happy to pay (Deloitte)

Here's the counterintuitive part: In India, South East Asia and China, 72-84% would keep their car longer if it gets regular OTA updates.

This contradicts the "SDV as disposable car" thesis. Software extends lifespan. Through continuous updates, the car stays fresh longer. Feels new longer. Remains valuable.

Germans don't see it that way. Only 36% would keep their car longer because of software updates.

That's the fundamental difference.

In Asia, software is added value. Something that makes the car better. Keeps it fresh. Makes it more valuable.

Germany sees software as nice to have. Many reject it completely.

The US falls in the middle.

My Take

The study shows 3 fundamental shifts. They lead to one central problem.

1) Germany becomes a discount market. China becomes premium.

For decades, it was reversed.

Chinese brands have good prospects in Europe. They offer good quality at affordable prices. Exactly what customers want.

In China, it's opposite. Performance, technology, and features count. Brand loyalty? Barely exists. 67-72% of customers in China, India, and Southeast Asia plan to switch brands with their next purchase.

German manufacturers must convince with technology. That's exactly what Chinese competitors deliver right now.

2) The big shift to EVs isn't coming in 2026 either.

Most customers aren't convinced yet. Hybrids remain the stronger alternative.

Betting only on pure EVs means missing 50%+ of the market. Manufacturers with strong hybrid portfolios win.

3) Asia wants software. Europe doesn't.

Deloitte says growth no longer works through higher prices and more new cars. The key lies in monetizing the existing fleet. That happens primarily through software.

The problem in Europe: home markets won't pay for it. Mostly aren't even ready for it. As a German OEM, you must invest in software. But you can't monetize it at home.

This brings us to the core problem.

The German home market is almost hostile to technology.

German car buyers are conservative. They adopt innovations late. They reject new technologies at first.

This is a cultural factor. It becomes a competitive disadvantage.

In the automotive business, a strong home market was always key to global success. The home market was the lab. The breeding ground for technology leadership.

German automakers developed high-tech in Germany for decades. Then carried it to the world.

But when home market customers think completely differently than the rest of the world, that itself becomes the problem.

This is the Chinese structural advantage. They have an extremely tech-friendly home market. What works in China also works in India. In South East Asia. In many rising markets.

Germany can't do that. The home market is closed. Critical. Technology-skeptical.

The success model no longer works.

Growing alienation. Between what the global market wants and what German customers want.

This explains why more development moves away from Germany. What works there doesn't work in the rest of the world.

German customers increasingly complain that cars no longer meet their expectations. Not because automakers aren't evolving. Because they develop for a global market that wants high-tech in a home market that rejects exactly that.

The question: Can German manufacturers serve both markets? Or must they choose?

That’s all for today.

Until next week,

Philipp

PS: If you find value here, share it with someone who should read it too.

Want to reach European automotive decision makers?

I help global B2B companies connect with 80,000+ automotive decision makers in Germany.