- The German Autopreneur

- Posts

- Goodbye Germany. VW Builds Its Future Elsewhere

Goodbye Germany. VW Builds Its Future Elsewhere

Philipp Raasch

March 21, 2026

Ad

BMW is in better shape than any other German automaker right now. One reason: its marketing team.

Uwe Dreher is Head of Marketing Europe at BMW. He completely transformed the division in 3 years.

In an interview with Jonas Wagner from Berylls by AlixPartners, he explains exactly what he changed.

→ How a unified KPI set makes performance across 25 countries manageable.

→ Why BMW had to restructure its own organization to keep pace with its own agency.

→ Where BMW already uses AI in marketing. And what it delivers.

Welcome to Issue #109 of The German Autopreneur.

VW reported earnings last week. Profits more than halved. Revenue stayed flat. So it's not about demand. It's about costs.

Operating margin: 2.8%. The last time it was this low? Dieselgate. Except now there's no scandal.

50,000 German jobs gone by 2030.

But we all know the numbers by now. What's more interesting is what VW CEO Oliver Blume said about them:

"The business model of past decades no longer works. Not for Volkswagen. Not for the German automotive industry. Not for Germany as a whole."

That's either a brutally honest diagnosis. Or Blume is turning a VW problem into a Germany problem.

Today I'm figuring out which one it is.

What was this business model? Why did it break? What's VW doing about it? And why that won't save Germany.

The Key Numbers

Group

Revenue: €321.9 billion (-0.8%)

Sales volume: 8.98 million vehicles (-0.5%)

Operating profit: €8.9 billion (-53%)

Operating margin: 2.8% (prior year: 5.9%)

One-time charges: ~€9 billion (Porsche ~€5B, tariffs ~€3B, restructuring ~€1B)

Porsche & Audi

Porsche operating profit: €90 million (prior year: €5.3 billion)

Audi operating profit: -13.6%

Porsche sales in China: -26%

So much for the numbers. Now for the question behind them.

What Was This Business Model?

The German business model in automotive worked like this for decades: Build highly complex machines at expensive locations and sell them worldwide at a premium.

A combustion engine has over 2,000 moving parts. Transmission, injection, exhaust treatment. This complexity was the moat. Master it, and you could charge more. Germany mastered it better than anyone.

Add cheap energy. Russian gas kept electricity prices low. Germany had high wages but stayed competitive overall.

Then China. For decades, THE growth market. Economic boom, rising middle class, more cars on the road every year. And no strong domestic auto industry. The jackpot for German automakers.

VW held over 40% market share there at times. The joint ventures printed billions.

These profits didn't just fund European investments. They kept the entire apparatus running. Overhead, bureaucracy, inefficient structures in Wolfsburg.

The formula: Complexity as moat × cheap energy × China profits = Made in Germany.

This formula worked for decades. Until all 3 variables collapsed at once.

Why Germany's Formula No Longer Works

1) The moat is dissolving An electric motor has about 20 moving parts. No transmission. No injection. No exhaust treatment. The complexity German automakers mastered better than anyone? Now irrelevant. Value creation is shifting to software and batteries.

2) The energy foundation is gone Russian gas is gone. Industrial electricity in Germany costs roughly twice as much as in China.

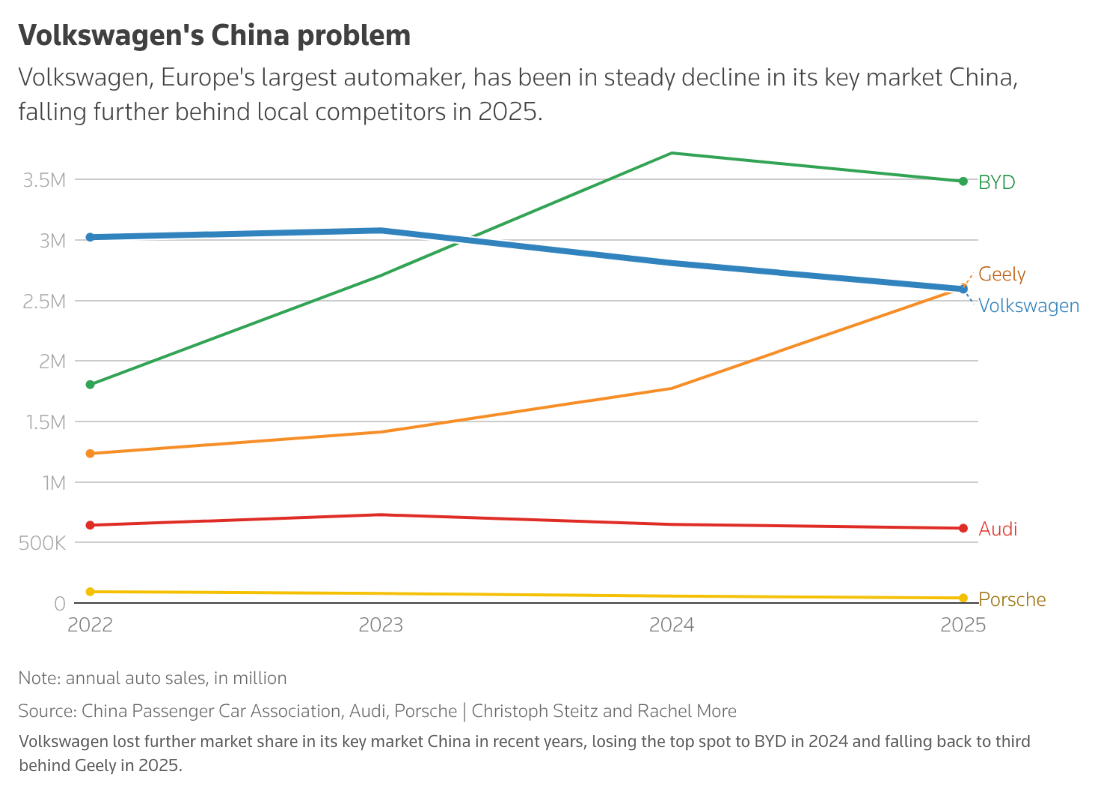

3) China isn't coming back VW was once number 1 in China. Today, number 3. Sales only fell 6% in 2025. But profit from joint ventures nearly halved: from €1.7 billion to €0.96 billion. At the peak, €5 billion per year from China alone. For 2026, VW expects only €200 to 600 million.

VW sales in China vs. local competitors 2022–2025 (Reuters)

China now has its own auto industry. One that barely existed 10 years ago. Local manufacturers like BYD and Geely understand the Chinese market better, build faster and cheaper.

For VW, the China curve pointed up for decades. Now it points down. And there's no bottom in sight.

How Did China Pull This Off?

This wasn't an accident. China's government recognized EVs as a strategic opportunity. The starting advantage: the world's largest car market as home turf. Demand was there. What was missing was domestic supply. So they built it. Around $230 billion in government subsidies flowed into the entire value chain. From raw materials through battery production to finished cars.

Europe reacted too. Just differently. Instead of building supply, they subsidized consumption. Germany offered €9,000 purchase incentives for EVs. When those ended in late 2023, the market collapsed. The irony: these incentives helped finance exactly the industry China was building. Because batteries in European EVs nearly all come from China.

Europe promoted a market. China built an industry.

This also explains why tariffs won't solve the problem. Tariffs protect existing structures. When the existing structure is the problem, you're protecting the problem.

Is Blume Right?

Back to Oliver Blume. He says this isn't a VW problem. Is that true?

The evidence supports it:

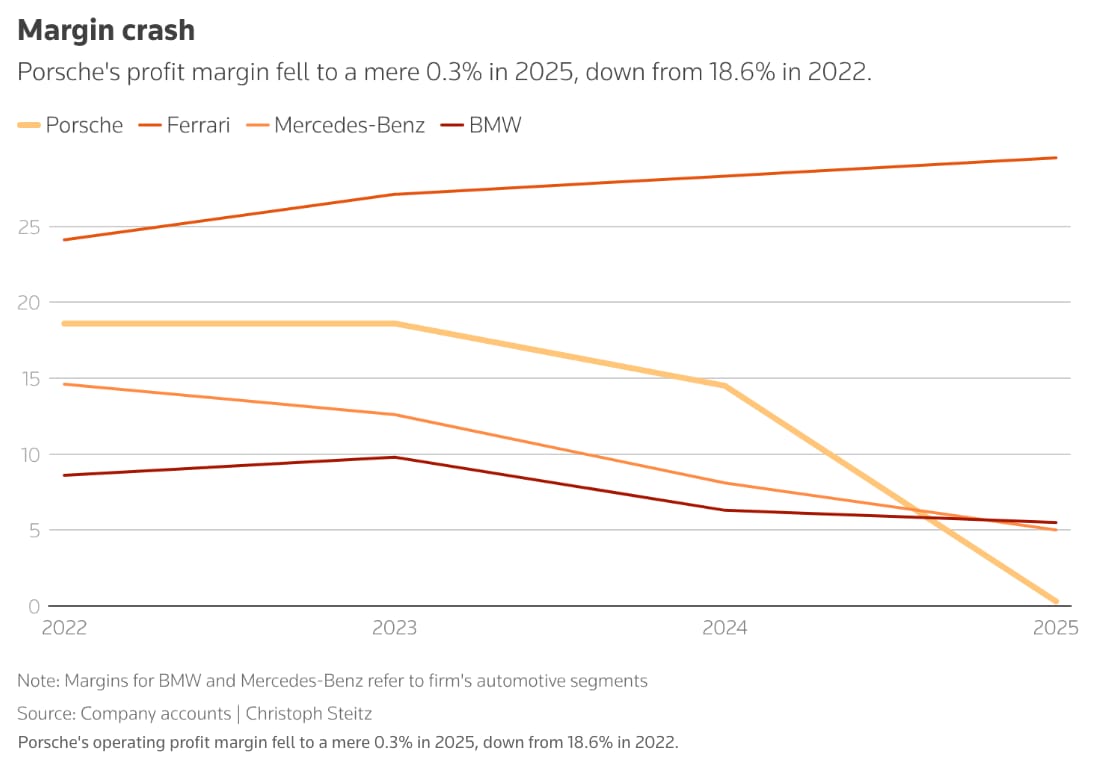

Mercedes: operating profit -57% in 2025

BMW: -11.5%

German automotive has cut over 100,000 jobs since 2019

Premium segment margins, 2022–2025 (Reuters)

So it's not just VW. But Toyota achieved 8.6% operating margin in the same environment. The Hyundai/Kia Group: 6.8%.

What separates German automakers from Toyota comes down to 2 things:

Disproportionate dependence on China

Strategic back-and-forth

And we see this at VW too:

First all-in on EVs. Then back to combustion

Build software ourselves with CARIAD. Then buy it instead

Develop platforms ourselves. Then partner with China and the US

So both are true. The formula no longer works. But VW also has a VW problem.

Can the Business Model Work Again?

Yes. But not with the old formula.

VW sold almost as many cars in 2025 as the prior year. 8.98 million, only -0.5%. In Europe, up 5%. In South America, up 10%.

And the powertrain mix tells a story that often gets lost. VW sold roughly 55% more pure EVs in 2025 than the year before. EV market share in Europe: 27%. More than combustion.

This isn't a dying company. This is an expensive company.

But the most important change: VW fundamentally flipped its strategy. Away from "do everything ourselves." Toward partnerships. With Rivian in the US. And with Xpeng in China.

VW is moving development away from Germany. Into regional hubs. Cheaper, faster, and closer to customers.

So VW is finding its answer.

But the answer is: somewhere else. The VW of the future isn't a German company anymore. It's a company with German roots.

But then what about the 'German business model' Blume talked about?

My Take

Oliver Blume built the perfect narrative. VW isn't the problem. Germany is the problem. And he's partly right. But he's leaving out the punchline. VW is solving its own problem. And leaving Germany to deal with its own.

There's no answer for that yet. Right now everyone's pointing at everyone else.

Automakers point at politics: expensive electricity, too much bureaucracy, no stable framework. Politicians point at companies: slept through transformation, clung too long to combustion. Unions point at management. And all of them point at China and Trump.

Every accusation probably has some truth to it. But that's exactly the problem. While everyone's busy pointing fingers, no one's working on an answer.

In the 1970s, British Leyland was the UK's biggest automaker. Dozens of brands under one roof: Jaguar, Rover, MG, Land Rover, Mini. Basically the VW of Britain.

But there were structural problems. Costs too high. Too much bureaucracy. Too little innovation. Instead of acting together, management, unions, and government blocked each other for years.

And while they fought, customers simply bought other cars. From Japan. And from Germany. Today, Britain has no mass-market manufacturer left.

Germany isn't there yet. But the beginning looks similar.

VW found an answer. But not for Germany.

Which means the last hope is gone. Legacy automakers won't reinvent Germany's business model.

That takes new players. Companies that don't exist yet. But for them to emerge, the whole system needs to work. Industry, politics, society. Together.

China keeps proving it can be done. But it doesn't happen on its own. It has to be orchestrated.

If it doesn't, companies will figure it out alone. By leaving. Just like VW is doing right now.

The question isn't whether Germany's business model can still work. The question is whether anyone will build a new one.

That's all for today.

What did you think of today's email? |

Feel free to reply to this email with your thoughts.

Until next week,

Philipp

PS: If you find value here, share it with someone who should read it too.

Want to reach European automotive decision makers?

I help global B2B companies connect with 80,000+ automotive decision makers in Germany.

I’m Philipp Raasch.

Ex-Mercedes. Now I help 80,000+ automotive professionals make sense of the industry's biggest transformation.